December 18, 2023

It’s nice to see the markets finally moving higher in a broad and inclusive way. Regular readers know that market gains prior to mid-October were largely the product of only 7 stocks, the mega cap technology names that you hear every day in the news. But since October 27th, everything changed for the better and suddenly diversified portfolios and value oriented investment strategies, like ours, are ripping higher. For this final update of 2023, I’m going to take the pulse on all things financial. My intent is not to forecast as much as highlight where things stand today on issues like markets and the economy, housing and mortgages, spending and saving, and of course, investor behavior. I’ll finish with some practical observations regarding the art of Financial Planning.

The Last Dance – Just Like We Said on October 9th

To be clear, this rally in global bonds and stocks, was not difficult to predict. We did so explicitly way back on October 9th in the blog post called The Last Dance. I’ll copy and paste the relevant text below as a reminder.

During the 4th quarter, I expect we will see the following:

- A quick recovery in stocks from the July-Sept sell off that ultimately gives way to the longer-term bear market in place since December of 2021.

- Bonds should form a bottom here and begin rising stronger than most would expect.

- Commodities and inflation beneficiaries should participate in the year-end rally but lag, especially as we close in on January.

- Internationals should rip higher if the dollar begins to sell off.

- Economic reports will continue to come in weaker than expected this quarter.

- We will see a peak in corporate earnings this quarter.

- We will see a peak in employment and wages.

- We will see real estate prices fall as supply finally arrives.

- There is a high probability that the Fed is done raising rates.

Ok, so that’s a pretty accurate assessment of what has actually happened in the last 9 weeks. The point is NOT to beat my chest and say I told you so. The point is to show that the action in the markets and where we are in the economic cycle are happening exactly as they typically do as the economic cycle starts over at Stage 1 (feel free to reread The Last Dance update for more detail).

Recession or No Recession?

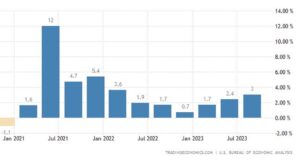

The probabilities are nearly 100% for a recession to occur in the US some time in 2024 but that is still just a probability. It’s also just a matter of semantics honestly. Recession is technically two consecutive quarters of negative GDP. We actually saw that happen in the first two quarters of 2022. You can see in the chart below that annual (year over year) GDP fell to 0.7% in Q4 of 2022.

Maybe that’s as close as we get to recession? Today, factually, economic growth is stable in aggregate and inflation is coming down quickly. Markets love that set up. We heard as much from the Fed this week. And predictably, stocks and bonds exploded higher in relief. Relieved from what? Relieved that the worst of inflation is behind us. What we do not know and haven’t seen yet are the lagging effects of inflation and the Fed’s historically late tightening cycle. They are only one week away from telling the markets that they are likely done raising rates and several quarters away from recognizing the lagging effects of said rate hikes. Remember the facts of the past.

Maybe that’s as close as we get to recession? Today, factually, economic growth is stable in aggregate and inflation is coming down quickly. Markets love that set up. We heard as much from the Fed this week. And predictably, stocks and bonds exploded higher in relief. Relieved from what? Relieved that the worst of inflation is behind us. What we do not know and haven’t seen yet are the lagging effects of inflation and the Fed’s historically late tightening cycle. They are only one week away from telling the markets that they are likely done raising rates and several quarters away from recognizing the lagging effects of said rate hikes. Remember the facts of the past.

- There is always a pause in Fed policy after a protracted period of raising interest rates and before they begin lowering rates. The minimum Pause historically has been 7.25 months, 218 calendar days or 150 market days. This is the minimum.

- The last rate hike was July of 2023. We are now 142 calendar days into the Pause.

- The Fed starts dropping interest rates when there are clear signs of recession, not before.

All things considered, I’m going to guess that we don’t have any clear signs of recession until the 2nd half of 2024 and that will be the time when the Fed starts to drop interest rates, not sooner.

So, dear investors, we have a nice relief rally happening now and we’ll enjoy the ride for as long as it lasts. We are fully invested and have been since the middle of October. But it’s important to understand the context of why this is happening now and our position in the economic cycle.

Housing and Mortgages

As of Friday, mortgage rates dropped below 7%. I found plenty of quotes, for those with a near perfect credit score, of 6.90% here in Colorado. That feels like a step in the right direction and mortgage rates should continue to drop predictably from here. Is 6.90% enough to entice buyers to act?

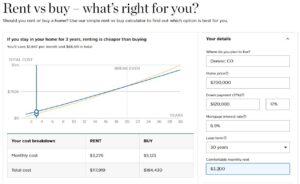

Honestly, we can’t answer that question in aggregate because people buy and sell homes for a variety of reasons, only one of which is related to borrowing costs. However, there is one giant comparative variable that is often used as an affordability benchmark and that is rental equivalencies. The question as always, should I rent or buy? This is a fun Rent v buy calculator tool from Nerd Wallet that I like to play around with. I entered a bunch of data for Denver which you can see on the right side. All pretty accurate for a single-family home, rents and today’s mortgage rates. Here’s the output.

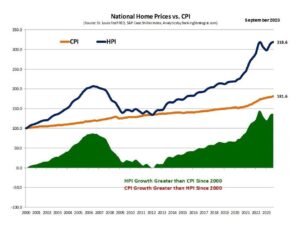

Ouch, ok so the breakeven today in Denver, CO. is about 28 years out. Meaning, even though mortgages have dropped below 7%, home prices are still way too high, and rents are still comparatively low. The Wall Street Journal ran an article with the same assessment and the same conclusions yesterday. Best to stay in that rental young lady, until rates fall closer to 5% or prices come down ~15-20%. The American Dream is still alive and well, but it looks like a good entry point is still a ways out. Of course, if you are paying with all cash or find something that is a screaming deal, have at it but keep in mind that prices are still working their way back down to the long term price trend (historically CPI) according to Bankingstrategist.com. Millennials and Gen Zs are well aware of this fact and we’re seeing the average age of first time home buyers move closer to 40 years old for the first time in history. They are none too pleased about it.

Ouch, ok so the breakeven today in Denver, CO. is about 28 years out. Meaning, even though mortgages have dropped below 7%, home prices are still way too high, and rents are still comparatively low. The Wall Street Journal ran an article with the same assessment and the same conclusions yesterday. Best to stay in that rental young lady, until rates fall closer to 5% or prices come down ~15-20%. The American Dream is still alive and well, but it looks like a good entry point is still a ways out. Of course, if you are paying with all cash or find something that is a screaming deal, have at it but keep in mind that prices are still working their way back down to the long term price trend (historically CPI) according to Bankingstrategist.com. Millennials and Gen Zs are well aware of this fact and we’re seeing the average age of first time home buyers move closer to 40 years old for the first time in history. They are none too pleased about it.

Spending and Saving Trends

Luxury goods, leisure travel, hotels, airlines and experiential spending are all very strong today. I laughed out loud when I saw this (nothing against Tata- she’s awesome!).

I laughed because the Time Person of the Year should be Consumer Spending! That is what Time is really pointing to when Taylor Swift is HER and personally responsible for $3 Billion in economic activity in the US in 2023. Wow.

I laughed because the Time Person of the Year should be Consumer Spending! That is what Time is really pointing to when Taylor Swift is HER and personally responsible for $3 Billion in economic activity in the US in 2023. Wow.

In other spending news. On-line sports gambling is on the rise, like a rocket. A few stats for you:

- 1 in 4 adults over 18 now describe their sports betting activity as regular.

- 42% of all sports betters, gamble daily.

- Daily gamblers spend on average more than 50% of their monthly take home earnings on bets.

- Only 3% of sports gamblers make money each year.

- ONLY 3% OF SPORTS GAMBLERS MAKE MONEY EACH YEAR (in case you missed it the first time).

- On-line sites like Draft Kings are required to report your winnings to the IRS, but not your losses. Ouch!

- Money spent on Sports Gambling in 2022 was $7.56 Billion, up from $920 Million in 2019.

- 85% report that sports gambling improves their lives. Good entertainment I suppose?

Hmmmm, so that’s a new spending trend.

Other spending categories are really the same as ever except everyone is still spending more money to get the same stuff like cars, food, electricity, trash, water, energy, healthcare, construction materials, etc.

What do we make of all this?

Well, we know that spending is still robust especially in luxury and fully discretionary type consumption. I see quite a bit of YOLO behavior (You Only Live Once) combined with a wealth effect from those who have benefited from the growth in asset prices like stocks and real estate. I also see a rather enormous pile of savings in the form of M2 (bank accounts, money market funds, CDs, etc). This has been growing exponentially since COVID. When we have cash available at our disposal, we tend to spend it. I certainly hope the Millennials and Gen Zs aren’t spending their future home down payment dollars?

Today, unfortunately, this is also happening.

And we are seeing credit card delinquencies rising strongly now but from a 5 year low.

And we are seeing credit card delinquencies rising strongly now but from a 5 year low.

So, I’m not sure what to make of all that but it does seem obvious that the Time Person of the Year curse might point to 2023 as the year of peak consumer spending in the US. After all Trump and Elon Musk were both Persons of the year at the peak of their power and popularity.

Investor Behavior

Charles Munger was famous for saying that investors are driven by Envy not Greed. He is 100% right. This too feels like an important moment in time for investors to really consider their individual goals, their needs and their personal risk tolerance. During periods like these, Envy investing drives bad decision making when we feel like we have failed if we are not making more than…. (your neighbor, some index, or something we heard on CBNC). We find ourselves chasing short term momentum and naturally we become more impatient, ignoring things like valuations. Yes Virginia, valuations are real, and they matter! Regular readers might recall our post called “40% Off Rack”. We have been beating the drum since mid-October about the incredible discounts in stocks, sectors and certain asset types, still trading at 40-50% below the highs of 2022. And yet, I continue to see more and more money plowing into stocks and sectors that have already moved up more than 200%.

So, where things stand today, investors would be very wise to considering digging deep for those discounts, perhaps trimming big winners, and getting those portfolios rebalanced, rediversified, and ready for 2024.

The Art of Financial Planning

When I was 21 years old my mother gave me an interesting gift. It was a session with an astrologer who was going to predict my future. I can remember very little about events or conversations I had at the age of 21 but I do clearly remember what this man told me. It has haunted me ever since. He told me that I would reach the peak of my career at age 42. What a terrible thing to say to a 21 year old. I don’t even know what “peak” means. Peak happiness? Peak income? Peak skills? 42 years old came and went but throughout my life, I have often benchmarked my career assessment on that arbitrary prediction. We all have a human interest in knowing the future, especially our own futures. Financial planning and all the algorithms we employ to predict our future, do a reasonable job of projecting and forecasting our financial well-being all the way out to our death. Our team of wealth managers including our Certified Financial Planners, work diligently to help you make life decisions like do I have enough to retire? Can I afford that house? How much do I have to save for my kids’ College Education? But as Carl Richards likes to illustrate:

There are a few important takeaways I would like to leave with you.

There are a few important takeaways I would like to leave with you.

- Planning is as much of an art as a science. Optimizing is elusive and we need to stay flexible regarding any predictive work.

- Planning is not something that is One And Done. The practice is best done regularly and especially when one has significant life changes like pending retirement, death, divorce, a liquidity event with company stock, a new child, etc.

- The All Season business model is built to encourage regular consultation with our certified financial planning partner, Kristi Sullivan. We charge a low asset based management fee (1.1% on average) for comprehensive wealth management that includes full discretionary asset management, tax preparation, up to 4 hours of annual financial planning and periodic updates to your estate with our attorney partners.

This is a clear value to our clients relatively and absolutely. But most importantly, our business model gives our team the opportunity to show you what the art of financial well-being really means.

I hope everyone has a happy and healthy holiday and we look forward to serving you in 2024!

Cheers

Sam Jones