“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.”

― Albert Einstein

Investors would do themselves a huge favor by spending a little time on the basic math behind compound returns. We tend to forget why this is important until we start to recognize risk and volatility in our investments. It is never too late to revisit the 8th Wonder of the World and apply the concept to concrete investment ideas like dividends, risk management and real wealth accumulation over time.

The Math – Average Returns versus Compound Annual Growth Rates (CAGR)

Let’s give a quick example and then explain the results.

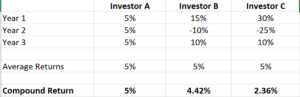

Please excuse the crude spreadsheet but the numbers are accurate.

Above we have three investors (A, B and C). Each investor has a different portfolio of holdings. Investor A earns a fixed return of 5% during each of the three years. Investor B has a portfolio that earns the SAME average return mathematically, over the three years but does so with a more volatile series of returns. And investor C has a Robinhood account, owns crypto currency and is swinging for the fences with unproven growth stocks. Still investor C, generates the same average return of 5% on paper despite the increased volatility. But each of these investors do not actually experience the same real returns as in returns that they can spend each year. The Compound Annual Growth Rates (CAGR) for each investor are shown above. Investor C clearly earns a lower real compound return compared to Investor A or B. Think of CAGR as the real returns that an investor earns on their investments and might be able to spend to offset living expenses. Average returns are mathematically deceptive because they do not reflect an investors’ real experience, wealth or purchasing power. Why does higher annual volatility in a portfolio reduce compound annual returns? I’m glad you asked.

The Merciless Math of Losses.

Quiz – If I lose 50% of my investment during a bear market, how much of a RETURN is necessary to break even?

Answers:

- 50%

- 100%

If you chose Answer B, then you understand it takes a greater return than the amount lost to break even due to the fact that you have less capital working for you at the lows of any decline. If I had $1 and lost .50 cents, I would need to make back .50 cents just to break even, right? (100% return on .50 cents)

The greater the loss, the greater the return needed to just break even. Think of all those stocks like Peloton that lost 97% recently. It would take a return of over 900% just to break even if you lost that entire amount (not in your lifetime, that company will be bought shortly). Many stocks these days are down well over 60% including some giants like Netflix. Indeed, these are lessons to be learned the hard way for some.

Implications for All Investors

The point of this critical lesson in financial literacy is this. If we want to improve our Compound Average Growth Rate (CAGR), which is the only true measure of wealth accumulation over time, we should constantly focus on building portfolios that earn consistent returns over time and find ways to mitigate or reduce annual volatility. Ok, so how do we do that? What tools do we have in our process, our selection or portfolio design that will help generate consistent returns (aka high CAGR)?

CAGR Seeking Investment Solutions

- Own dividend and income generating securities.

I can’t say enough about the value of earning dividends and income in any investors’ portfolio. Consider this. In the last two calendar decades (12/31/1999 – 12/31/19), the S&P 500 index with dividends earned a Compound Annual Growth Rate of 5.98%. Without dividends that number was only 4.03%. Dividends accounted for exactly 33% of the total returns over time. I would not personally consider the S&P 500 to be a high dividend index, but it does have a history of paying between 1.5 and 2% annual dividends as an index. Now imagine over a long period of time what we might generate in CAGR if we invested the bulk of our capital in an actual high dividend ETF or index. We own many of these in our All Season strategy so I’ll list a few holdings and their current annual dividend rates.

- Ishares Core High Dividend ETF (HDV) 3.47% annual dividend yield

- SPDR S&P High Dividend ETF (SPYD) 3.72% annual dividend yield

- I Shares Select Dividend ETF (DVY) 3.24% annual dividend yield

*All three ETFS above are positive YTD by 7-9% in a market that is down double digits.

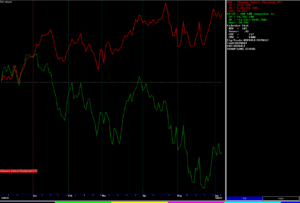

Chart of DVY (shown in Red) versus the S&P 500 (shown in Green) YTD.

Already we are seeing high dividend paying securities outperforming the markets in absolute terms but importantly they are also generating their returns with far less daily and weekly volatility than the market. This is an example of consistency and the benefits of real CAGR results at its best!

For what it’s worth, our MASS income strategy which focuses 100% on high Dividends and Income generated from stocks, alternatives and bonds, continues to generate an annualized yield of over 6%. I’ve said this before but this is just gold in an inflation driven environment like today.

- Diversify!

It is sort of sad to me to see how many investors are sitting with undiversified portfolios these days. I only see portfolios of stocks when new investors come to our firm. Never bonds, never gold, never alternatives, or non-correlated holdings. Always Technology, always concentrated positions and always a pile of identical stock index securities. Admittedly, bonds have not served their historical role as a good diversifier in the last two years as bonds have lost as much or more than stocks since early 2021. But, But, But! Bonds are now returning to their place in line. Bonds are beginning to behave themselves and actually move differently than stocks (non-correlation). That is a tremendous breath of fresh air. Gold is still moving in sync with stocks but historically has also been a great diversifier. Commodities are the real diversification winner in the last 24 months, as we know, but I never see commodities in anyone’s portfolios except for our clients. Some think Crypto currencies offer diversification. However, the evidence would suggest that Crypto is just negatively correlated to anything that goes up (wink).

Regardless, this is a great moment in time to revisit your asset allocation mix and make sure to truly, really, and honestly diversify your portfolio. If you need help as a DIY investor, please call us asap. The direction of the markets and economy from here is not going to be pleasant to investors who don’t get this right

- Risk Management

The final method of seeking consistency and a higher CAGR, is to trade away volatility and this is not something I would recommend unless you know what you’re doing. Very publicly, I reject the notion that this is impossible. We have 27 years of data and historical performance to prove it. People like Warren Buffet and George Soros have done so successfully for decades. Markets are inefficient enough and run to obvious extremes often enough that there are clear opportunities to “manage” volatility. Sometimes we want to reach for volatility, like at market lows. Other times we want to reduce our exposure to volatility at market highs. Of course, it can be done successfully and repeatedly, but it’s a ton of work and involves a lot of skill and experience. If you feel capable, have at it. If you want us to do it, call us. Otherwise, seek consistent CAGR returns with #1 and #2 above.

On the Main Stage

I’ll finish with a brief update on current conditions and trends as well as a few predictions which I am always reluctant to make. The economy is slipping toward recession. There is little doubt this is happening and the possibility of the Federal Reserve somehow avoiding a recession is nearly zero in my book. We are already beginning to see the labor market cool off with lower payroll numbers and slightly higher unemployment this month. More layoffs are coming in bulk, especially from the tech sector. Those who remain employed however will still be able to collect higher wages and salaries especially in higher skilled industries with high demand. I suspect the work from home thing might also be coming to an end for a lot of companies. It was fun while it lasted right? This is not the end of the world but rather a cyclical event that occurs every 5-7 years. We haven’t had a lasting recession in over 12 years so we’re way overdue.

Real estate is doing what it always does. Trends in pricing and sales tend to follow behind the stock market by 9-12 months so we would expect to see some weakness starting about now. You will likely hear about rising inventories of unsold homes, a shift from a seller’s market to a buyer’s market and some price declines in high flying areas of the country. Income properties, like fully occupied commercial or residential rentals, are really in the sweet spot against high and steady inflation, so those types of assets might continue to appreciate. This should not come as a surprise to anyone.

Meanwhile, the Fed is going to raise rates again by .50% next week on the 15th. They are driving the economy into recession, make no mistake. It’s the only way out of the inflation bubble we’re in.

Inflation is also starting to peak in terms of the rate. But remember, that inflation is only reported as a rate of change, year over year. If inflation goes flat from here and for the next 12 months, we will still be operating in an environment of very high costs of living. It is not until the inflation rate drops dramatically over a period longer than one year that we will really start to feel some easing in pricing pressures. In the end, as I indicated several months ago, we will probably have to wade through a tough cycle of “Stagflation” (stagnant economy with inflation), something like the 70’s.

The thing to remember as we move into this next stage of the economic cycle, is that it is just another season or cycle. There are opportunities and risks in every cycle. Our job is to be awake and alert to changes in the environment and simply allocate our assets and resources appropriately. Easier said than done but that why we are here to help.

That’s it for now. Summer is coming fast! Enjoy it.

Cheers,

Sam Jones